In nagenoeg elk gesprek over de toekomst van finance valt het woord data-driven. CFO's praten over realtime dashboards, predictive cashflow en AI die afwijkingen detecteert voordat de controller ze ziet. Het is een aantrekkelijk beeld — alleen klopt het zelden met de praktijk op de werkvloer.

Wat ik in de afgelopen vijftien jaar consistent zie: organisaties slaan stappen over. Ze willen AI-gedreven forecasting terwijl de standaardrapportage nog drie weken na maandafsluiting komt. Ze willen anomaly detection terwijl de hoofdboekstructuur per entiteit verschilt. Het resultaat is voorspelbaar: dure technologie, gefrustreerde teams, en management dat de cijfers nog steeds niet vertrouwt.

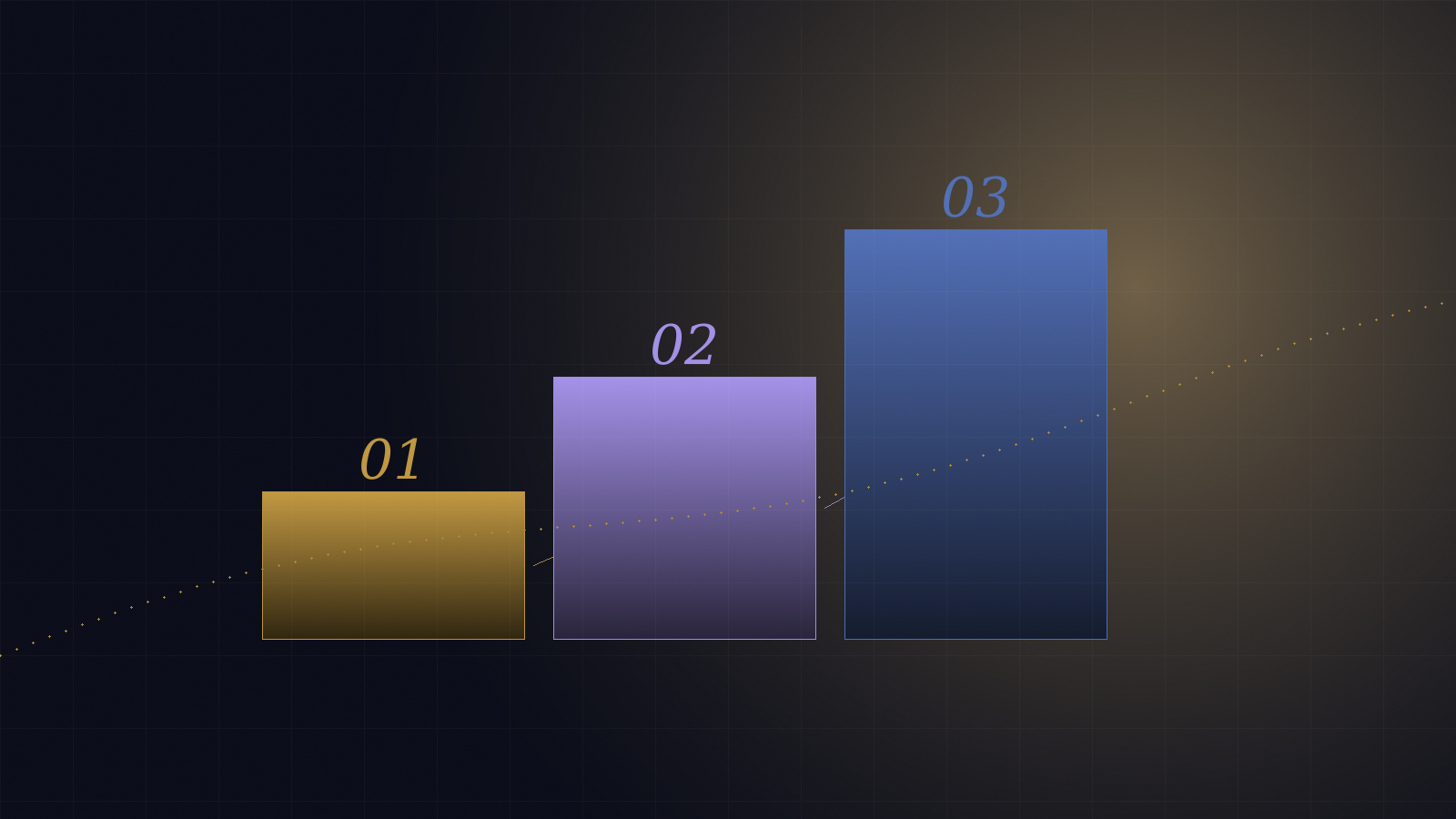

Het HAAI maturity-model lost dit op door drie niveaus te onderscheiden — en duidelijk te maken wat eerst af moet voor de volgende stap zinvol wordt.

Niveau 01 — Registration: het fundament

Op niveau één gaat alles om betrouwbare registratie. Het ERP-systeem reflecteert de werkelijkheid, de hoofdboekstructuur is consistent, de maandafsluiting is voorspelbaar. Basis-MIS is beschikbaar voor besluitvorming. Geen exotische technologie — gewoon een goed ingericht systeem en een team dat de processen volgt.

Klinkt eenvoudig. Is het zelden. In multi-entity organisaties zijn rekeningschema's vaak historisch gegroeid en niet gestandaardiseerd. Tussenrekeningen lopen op zonder periodieke analyse. Maandafsluiting kost twee tot drie weken omdat handmatige controles en correcties domineren. Op dit niveau is "datagedreven werken" een fata morgana — er is geen schone data om op te bouwen.

Wie hier inveert in AI bouwt prachtige dashboards op modder. De cijfers zien er goed uit en zijn toch niet bruikbaar.

De interventies op dit niveau zijn klassiek finance-werk: hoofdboekherstructurering, accounting manuals, geautomatiseerde reconciliaties, een strakke afsluitkalender. Niet sexy, wel fundamenteel.

Niveau 02 — Exception: sturen op afwijkingen

Met een betrouwbaar fundament verschuift de focus. Het team kijkt niet meer naar elke transactie — dat is overbodig — maar naar uitzonderingen. Welke posten wijken af van het verwachte patroon? Welke processen leveren consistent fouten op? Welke entiteit rapporteert steevast laat?

Op niveau twee gaat data-analytics een rol spelen, maar nog niet als AI. Power BI of vergelijkbaar toont KPI's met afwijkingsindicatoren. Reguliere queries vinden ongebruikelijke journalposten. De auditfunctie verschuift van "alle transacties controleren tot een grens" naar "afwijkingen identificeren en uitleggen".

Dit niveau levert vaak de grootste relatieve verbetering. Het werk wordt scherper en het team krijgt eindelijk tijd voor analyse in plaats van transactieverwerking.

Niveau 03 — Risk: AI-gedreven inzicht

Pas op niveau drie heeft AI iets nuttigs te doen. Met betrouwbare basisdata en begrip van uitzonderingen kan een model patronen leren die menselijke analisten missen — niet omdat de analist minder slim is, maar omdat de hoeveelheid data groter is dan een mens kan overzien.

Concrete toepassingen op dit niveau: predictive cash flow op basis van klantgedrag, AI die ongebruikelijke combinaties van journalposten flaggt, classifiers die inkoopfacturen categoriseren met een betrouwbaarheidsindicator zodat alleen onzekere gevallen menselijke aandacht krijgen. Statische rapportage wordt vooruitkijkend inzicht.

Waarom de volgorde ertoe doet

Een organisatie kan niet bewust op niveau drie gaan zitten zonder de eerste twee. Dat is geen dogma — het is een praktische vaststelling. AI op vuile data versterkt fouten in plaats van ze te ontdekken. Anomaly detection zonder begrip van wat normaal is, levert vooral ruis op.

Het goede nieuws: de stappen kunnen vaak parallel lopen. Terwijl een hoofdboek wordt gerestructureerd op niveau één, kan een ander team al aan de uitzondering-rapportage werken voor de afdelingen die wel op orde zijn. Het maturity-model is een richtinggevend kader, geen rigide watervalplan.

De vraag waar elke CFO mee zou moeten beginnen is dus niet "welke AI moeten we kopen?" maar "op welk niveau staan onze entiteiten en wat is per entiteit de eerstvolgende zinvolle stap?"